Video Game Market Growth by Game Type

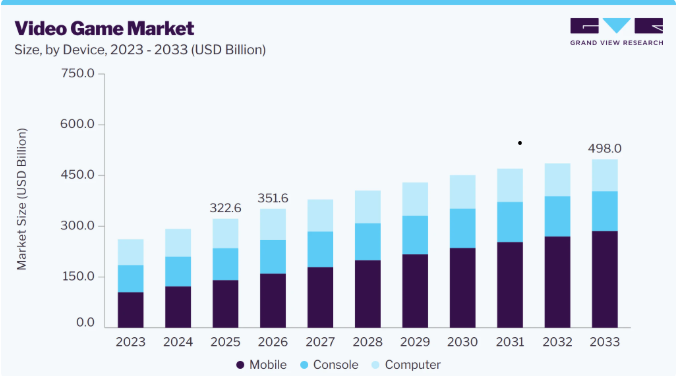

The global Video Game Market was valued at USD 322.6 billion in 2025 and is projected to grow from USD 351.6 billion in 2026 to USD 498.0 billion by 2033, registering a CAGR of 5.1% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 49.0% in 2025, driven by its massive gaming population, expanding smartphone adoption, robust esports ecosystem, and increasing investments in game development and digital entertainment.

The video game industry continues to evolve as technological innovation, cloud infrastructure, mobile connectivity, and immersive gaming experiences reshape how consumers engage with digital entertainment. Rising internet penetration, affordable gaming devices, and widespread smartphone adoption have expanded the global player base, while live-service games, multiplayer ecosystems, and digital distribution platforms continue generating recurring revenue for publishers.

Consumers increasingly seek interactive, social, and personalized gaming experiences across mobile, PC, and console platforms. Advancements in artificial intelligence (AI), cloud gaming, augmented reality (AR), virtual reality (VR), and real-time rendering technologies are enabling developers to deliver highly immersive gameplay while extending player engagement through continuous content updates and community-driven experiences.

Mobile Gaming and Cloud Platforms Driving Market Growth

Mobile gaming remains the fastest-growing segment of the video game market, supported by improvements in smartphone hardware, affordable mobile internet, and evolving monetization strategies.

Key technologies transforming the industry include:

- Cloud gaming platforms

- Artificial intelligence (AI)-powered game development

- Augmented Reality (AR)

- Virtual Reality (VR)

- 5G connectivity

- Cross-platform gaming ecosystems

Game developers are increasingly adopting mobile-first development strategies, designing games with intuitive touch interfaces, session-based gameplay, in-app purchases, subscriptions, and battle pass models that maximize player engagement and recurring revenue.

Cloud gaming is further transforming content delivery by enabling players to stream high-quality games without requiring expensive gaming hardware. Investments in cloud infrastructure, edge computing, and 5G networks are reducing latency while making premium gaming experiences more accessible to both casual and competitive players worldwide.

Emerging Industry Trend: Inclusive Design and AI-Driven Player Experiences

One of the most influential trends shaping the video game market is the growing emphasis on inclusive storytelling and accessible game design. Developers are creating culturally diverse narratives featuring inclusive characters, gender representation, and localized storytelling that resonate with global audiences.

Accessibility features are becoming standard across modern games, including:

- Customizable controls

- Colorblind modes

- Subtitle customization

- Adaptive user interfaces

- Assistive gameplay options

Simultaneously, AI-powered development tools are accelerating content creation by automating environment generation, character behavior, dialogue systems, and gameplay balancing. AI-driven personalization is also improving player retention through adaptive difficulty, intelligent matchmaking, and customized in-game experiences.

Key Market Trends & Insights

Mobile Gaming Dominates Device Segment

- By device, the mobile segment accounted for the largest market share of 43.7% in 2025.

- Affordable smartphones, expanding internet access, and continuous improvements in mobile GPU and CPU performance continue driving global adoption.

- Mobile platforms have become the preferred gaming medium across emerging economies, supported by free-to-play business models, in-app purchases, and digital payment integration.

Offline Gaming Maintains Strong Market Presence

- By type, the offline segment held the largest market share of 54.31% in 2025.

- Strong demand for immersive single-player experiences continues supporting offline gaming despite the rapid growth of online multiplayer titles.

- Developers continue investing in expansive open worlds, cinematic storytelling, advanced AI mechanics, and narrative-driven gameplay that can be enjoyed without continuous internet connectivity.

Looking for more specific insights? Customize this report to suite your business needs

Regional Highlights

- Largest Regional Market: Asia Pacific (49.0% revenue share, 2025)

- Leading Country: China

Asia Pacific remains the largest video game market globally due to its extensive gaming population, strong mobile gaming ecosystem, expanding esports industry, and increasing investments from leading publishers. China continues leading regional revenue generation through its massive mobile gaming audience, advanced digital payment infrastructure, and rapidly growing cloud gaming adoption.

Market Size & Forecast

- Market Size (2025): USD 322.6 Billion

- Estimated Market Size (2026): USD 351.6 Billion

- Projected Market Size (2033): USD 498.0 Billion

- CAGR (2026–2033): 5.1%

Growing investments in cloud gaming, AI-powered game development, esports ecosystems, and next-generation graphics technologies continue expanding monetization opportunities across the global gaming industry. The integration of AR, VR, blockchain, and real-time rendering technologies is creating richer player experiences while enabling developers to introduce new gameplay mechanics and digital economies.

The rapid expansion of streaming platforms, creator communities, and competitive gaming further strengthens long-term player engagement, transforming gaming into one of the world's fastest-growing digital entertainment industries.

Competitive Landscape

Leading companies operating in the global video game market continue investing in game development, cloud gaming infrastructure, AI technologies, esports expansion, strategic acquisitions, and live-service ecosystems to strengthen their competitive positions.

Major competitive strategies include:

- Live-service game development

- AI-assisted game creation

- Cross-platform gaming integration

- Cloud gaming expansion

- Esports ecosystem development

- Strategic acquisitions and partnerships

- Subscription-based gaming services

Activision Blizzard

Activision Blizzard continues to maintain a strong position in the global video game industry through blockbuster franchises including Call of Duty, World of Warcraft, and Overwatch. The company focuses on multiplayer experiences, live-service business models, seasonal content updates, and esports initiatives that generate recurring player engagement and long-term monetization. Its strong console and PC portfolio continues driving global brand recognition.

Tencent Holdings Ltd.

Tencent Holdings Ltd. remains one of the world's largest gaming companies through its leadership in mobile gaming, digital publishing, and strategic investments across the global gaming ecosystem. The company holds significant stakes in leading developers including Riot Games and Epic Games while continuing to invest heavily in cloud gaming, AI technologies, cross-border publishing, and esports infrastructure. Tencent's extensive digital ecosystem and strategic partnerships enable it to influence emerging gaming trends worldwide.

Emerging Market Participants

Rovio Entertainment Ltd. continues expanding its presence through casual mobile games led by the globally recognized Angry Birds franchise. The company focuses on cross-platform engagement, innovative monetization strategies, and brand expansion across merchandise and digital entertainment.

Lucid Games specializes in developing multiplayer and cooperative gaming experiences optimized for console and PC platforms. Its agile development model enables rapid adaptation to emerging technologies and evolving player preferences while strengthening partnerships with larger publishers.

Key Video Game Companies

The following companies are among the leading participants operating in the global video game market:

- Activision Blizzard

- Take-Two Interactive Software, Inc.

- Epic Games

- Electronic Arts Inc.

- Lucid Games

- Microsoft Corp.

- Nintendo

- Rovio Entertainment Corporation

- Sony Interactive Entertainment Inc.

- Tencent Holdings Ltd.

Conclusion

The global video game market continues to evolve through rapid technological innovation, expanding digital ecosystems, and growing consumer demand for immersive entertainment experiences. Mobile gaming, cloud gaming, esports, artificial intelligence, and next-generation graphics technologies are reshaping how games are developed, distributed, and monetized across global markets. Simultaneously, increasing emphasis on inclusive storytelling, accessibility, and cross-platform experiences is strengthening player engagement and broadening audience reach. As publishers continue investing in cloud infrastructure, AI-powered development, live-service ecosystems, and competitive gaming communities, the video game market is expected to maintain steady long-term growth while creating new opportunities across digital entertainment, interactive media, and connected gaming platforms.

Looking for a report customized to your requirements? Explore our Custom Research Offering

Grand View Research offers

- Focused market intelligence reports on specific geographies or high-growth segments

- Extended forecast timelines for long-term planning

- Competitor Benchmarking and Supply Chain Analysis

- Inclusion of regulatory and policy assessments

- Inclusion of custom data models, KPIs, or applications unique to your business

- Specific high-impact Data Decks and Tables to support effective decision making

And much more…